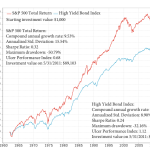

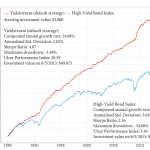

On our performance page, we present live and backtested results for the Yieldstream strategy beginning in 1984 — the earliest year for which a reasonably deep universe of high yield bond mutual funds is available. But the underlying market dynamics that our strategy exploits — credit cycles, mean reversion in yield spreads, and persistent momentum — are not artifacts of the modern era. They have been present in credit markets for as long as those markets have existed.

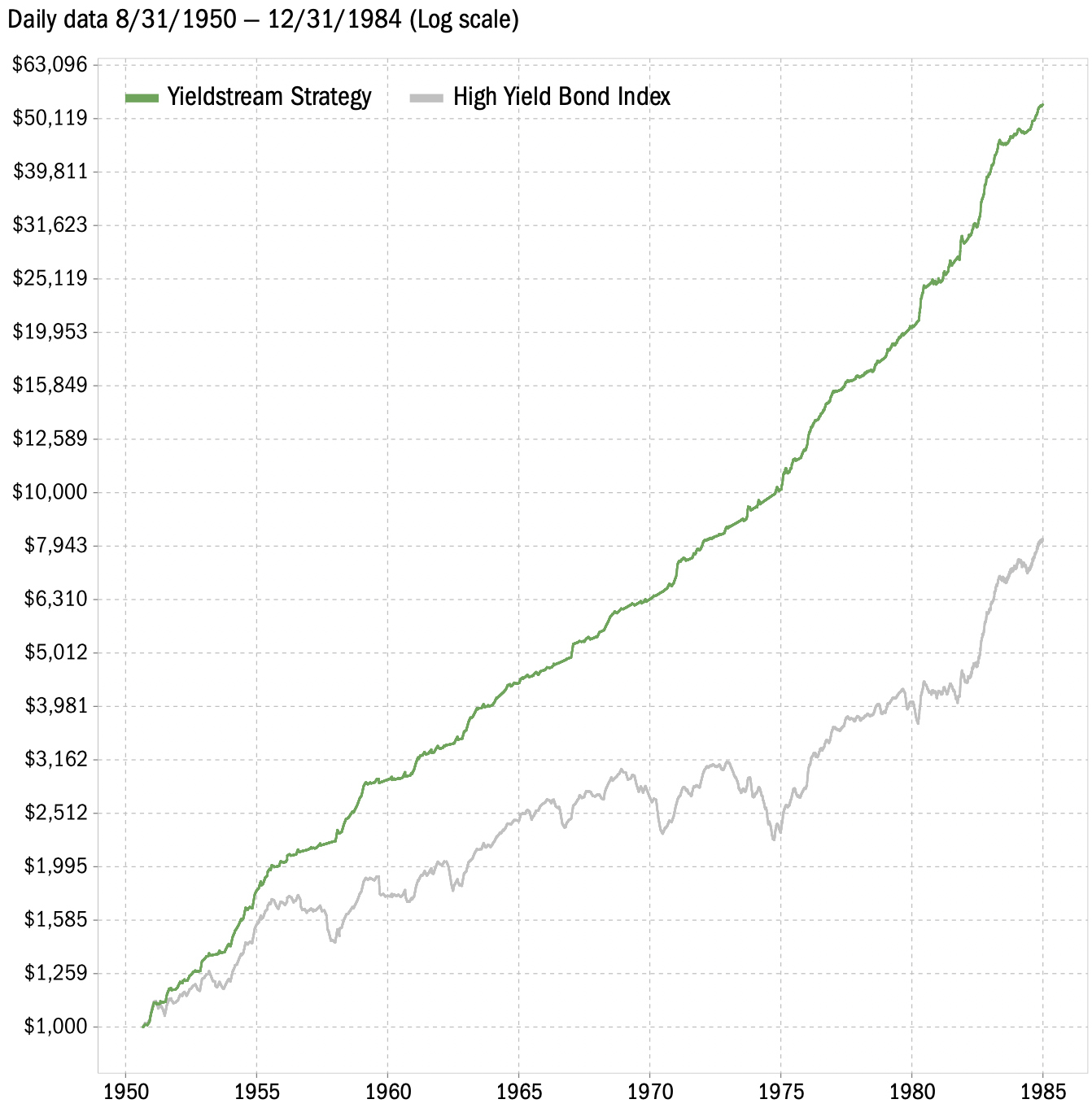

To test this, we extended our Yieldstream backtest to 1950, using the longest-lived high yield bond funds available: Northeast Investors Trust (NTHEX) and Allspring High Yield Bond Fund (EKHAX), which have been available since 1950, and 8 other High Yield Bond mutual funds which were launched between 1950 and 1984. The chart below shows the hypothetical growth of $1,000 invested in the Yieldstream strategy from 1950 through 1984, compared to a passive high yield bond allocation over the same period.

| Strategy: | Yieldstream | High Yield Index |

|---|---|---|

| Compound Annual Growth Rate | 12.3% | 6.3% |

| Standard Deviation | 1.7% | 2.9% |

| Maximum Drawdown | -3.1% | -28.5% |

| Sharpe Ratio | 3.79 | 0.36 |

| Growth of $1,000 invested in 1950 | $53,245 | $8,131 |

This backtest applies the same core systematic methodology and model specification that drives the Yieldstream strategy today. The signal generation logic, allocation rules, and risk management framework are identical to what Yieldstream subscribers rely on in live markets.

The results are consistent with what we observe in the post-1984 period: the strategy captures a large share of the upside during favorable credit environments while systematically reducing exposure ahead of significant drawdowns. Over this 34-year window, Yieldstream delivered a compound annual growth rate roughly double that of a passive high yield allocation, with materially lower volatility and substantially shallower drawdowns.

For any systematic strategy, out-of-sample durability is the most meaningful test of robustness. Overfitted models tend to degrade quickly outside the period in which they were developed. The fact that the Yieldstream methodology produces strong risk-adjusted returns across multiple decades — spanning different interest rate regimes, credit cycles, inflationary environments, and market structures — provides meaningful evidence that the strategy captures a durable and persistent source of return in fixed income markets.